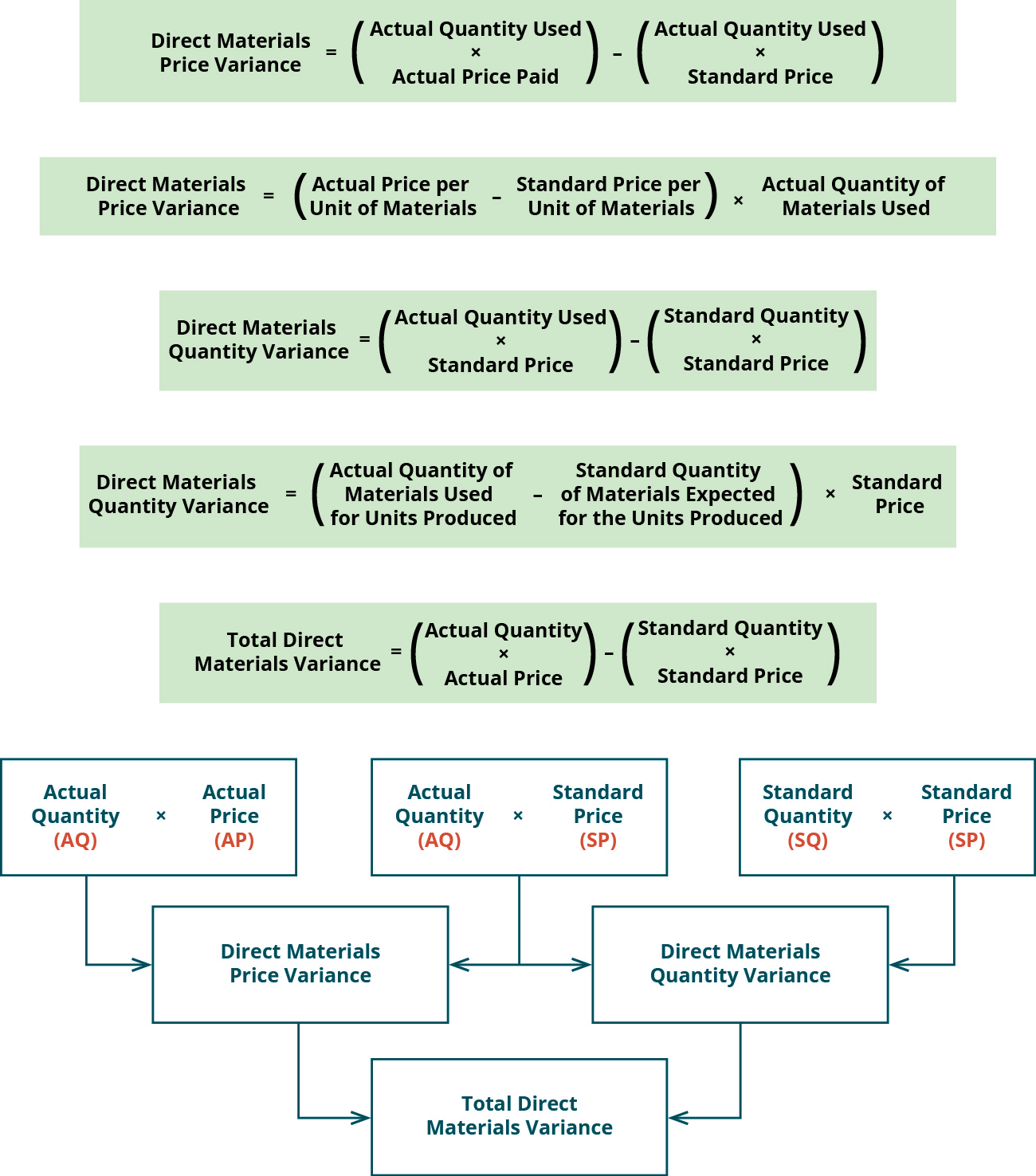

Direct Materials Price Variance Formula, Calculation & Example

Moreover, we have discussed the role of technology in reducing efficiency variance, common causes of efficiency variance, and best practices for addressing it in a manufacturing plant. Additionally, we have explored when a company should consider investing in new equipment, outsourcing certain processes, and how to ensure accountants that employees are adequately trained to minimize efficiency variance. Poor production planning can result in inefficient use of resources, leading to increased costs and reduced efficiency. For example, if a production process is not scheduled correctly, it can result in delays, overtime, and increased costs.

How to apply price variances to direct materials in cost accounting

Furthermore, by continuously monitoring efficiency variance and improving over time, companies can stay ahead of their competitors and maintain a competitive advantage in the marketplace. By reducing efficiency variance, companies can improve their bottom line, increase customer satisfaction, and gain a competitive advantage in their industry. This shows that we saved money by buying cheaper, but lost money because of material waste.

Regular Monitoring and Analysis – Best Practices for Addressing Efficiency Variance

- Total standard quantity is calculated as standard quantity per unit times actual production or 4.2 feet of flat nylon cord per unit times 150,000 units produced equals 630,000 feet of flat nylon cord.

- Actual manufacturing data are collected after the period under consideration is finished.

- Overhead efficiency variance examines the difference between the standard overhead costs allocated for a certain level of production and the actual overhead costs incurred.

- Since direct labor hours are the cost driver for variable manufacturing overhead in this example, the variance is linked to the direct labor hours worked in excess of the standard labor hours allowed.

- For example, IoT sensors can monitor the exact amount of material used in each production cycle, allowing for precise adjustments and reducing waste.

Meeting customer demands can improve customer satisfaction and help retain and attract customers. New equipment may incorporate technological advances that can improve efficiency and reduce variance. If competitors use more advanced equipment, investing in new equipment may be necessary to remain competitive.

What is the difference between labor rate and efficiency variance?

Big data analytics involves using advanced algorithms and machine learning to analyze large amounts of data and identify patterns and insights that would be difficult or impossible to see using traditional methods. The cost accountant is responsible for analyzing the costs of production and identifying areas where costs can be reduced. The cost accountant works closely with the production manager to ensure that production processes are optimized and that efficiency variance is minimized. A negative labor efficiency variance, on the other hand, means that the company has used more labor hours than expected, indicating that there may be inefficiencies in its processes. Then, you would multiply the quantity variance (-100) by the standard rate ($10) to get an efficiency variance of -$1,000. This means that the company was less efficient than expected, and the inefficiency cost them $1,000 in lost productivity or increased costs.

Actual data includes the exact number of units produced during the period and the actual costs incurred. The actual costs and quantities incurred for direct materials, direct labor, and variable manufacturing overhead are reported in Exhibit 8-1. The direct materials price variance of Hampton Appliance Company is unfavorable for the month of January. This is because the actual price paid to buy 5,000 units of direct material exceeds the standard price.

Outsourcing specific processes can allow a company to focus on its core competencies and strategic goals. This can help improve overall efficiency and reduce variance in areas critical to the company’s success. Efficiency variance can lead to non-compliance with industry regulations and standards.

By understanding and monitoring efficiency variance, companies can identify areas where they can improve their processes, reduce costs, and increase productivity. Implementing a robust quality control program can help to reduce efficiency variance. This involves monitoring and measuring product quality and identifying defects or issues. Quality control should be implemented at all stages of the manufacturing process, from raw materials to finished products.

Total direct material costs per the standard amounts allowed are the total standard quantity of 630,000 ft. times the standard price per foot of $0.50 equals $315,000. Per the standard cost formulas, Brad projected he should have paid $315,000 for the direct materials necessary to produce 150,000 units. Total standard quantity is calculated as standard quantity per unit times actual production or 0.25 direct labor hours per unit times 150,000 units produced equals 37,500 direct labor hours. Total direct labor costs per the standard amounts allowed are calculated as total standard quantity (37,500) times standard rate per hour ($18) equals $675,000.

Companies need to be agile and adaptable to mitigate the impact of these external factors on their efficiency. Another important factor is the quality of the materials and equipment used in the production process. High-quality materials and well-maintained equipment can enhance productivity by minimizing downtime and reducing the likelihood of defects. Poor-quality materials, on the other hand, can lead to increased waste and rework, negatively impacting efficiency. Similarly, outdated or poorly maintained equipment can cause frequent breakdowns, leading to delays and higher resource usage. Efficiency variance analysis is a critical tool for businesses aiming to optimize their operations.

Management can then compare the predicted use of \(600\) tablespoons of butter to the actual amount used. If the actual usage of butter was less than \(600\), customers may not be happy, because they may feel that they did not get enough butter. If more than \(600\) tablespoons of butter were used, management would investigate to determine why. Therefore, if the theater sells 300 bags of popcorn with two tablespoons of butter on each, the total amount of butter that should be used is 600 tablespoons. Management can then compare the predicted use of 600 tablespoons of butter to the actual amount used. If the actual usage of butter was less than 600, customers may not be happy, because they may feel that they did not get enough butter.

An unfavorable outcome means you spent more on the purchase of materials than you anticipated. This result is interpreted as the organization paid $30,000 more for materials used in production than they planned. This direct materials price variance could indicate a purchasing issue, such as the purchasing department paying more than the agreed-upon amount (purchase order amount).