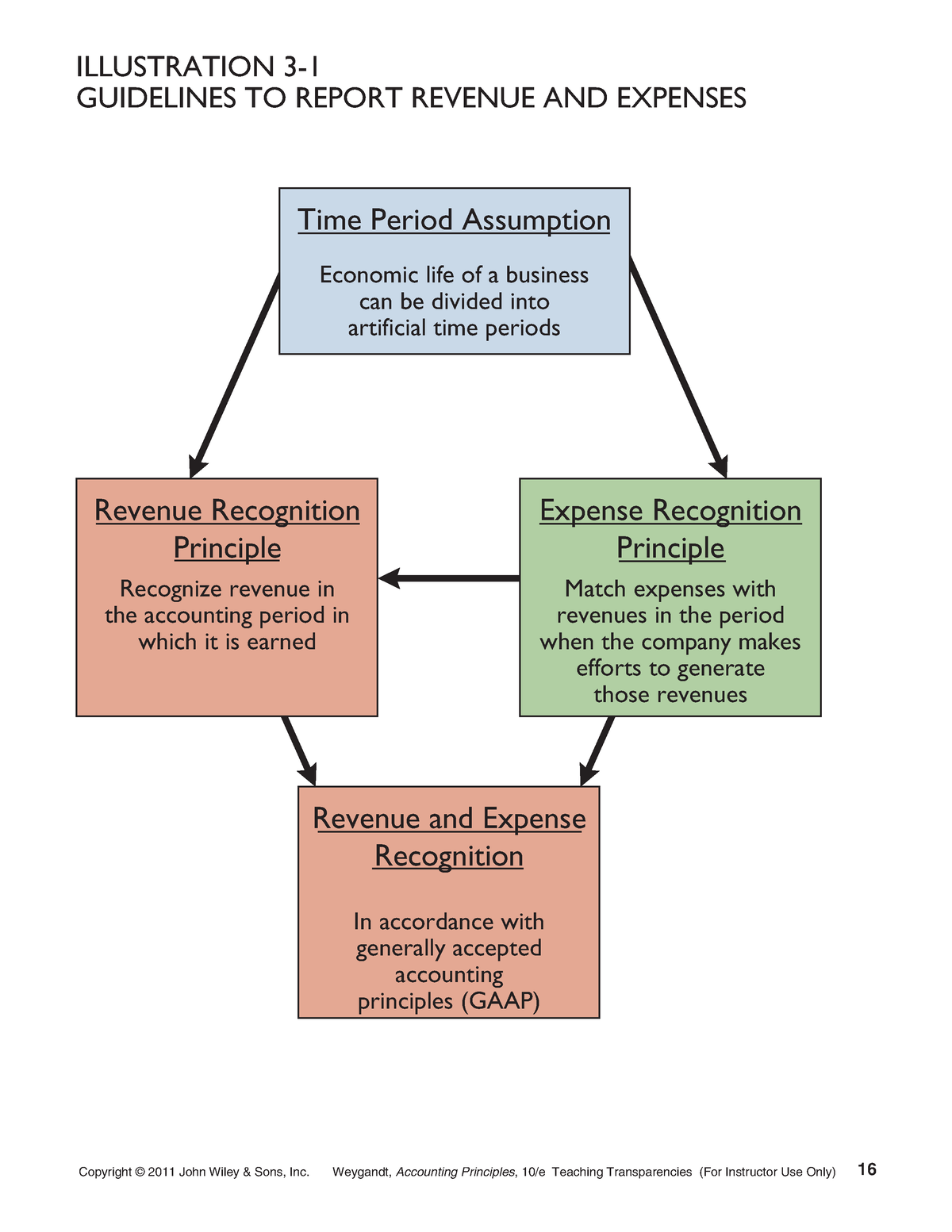

Time Period Assumption: Time Period Assumption: The Temporal Dimension of the Realization Principle

Under accrual basis, revenues and expenses are recognized when they occur regardless of when the amounts are received or paid. If you look at the header portion of the income statement, cash flow Statement and statement of changes in equity, you’ll notice that the accounting period is indicated below the financial statement names. It is usually written as “For the year ended December 31, 20xx” or “For the quarter ending March 31, 20xx”. This indicates the period covered in the financial statements and is useful when analyzing the financial statements across different periods. Basic accounting assumptions serve as the foundation of the accounting process and are derived from the experiences and practices of accountants. These underlying assumptions enhance the understanding of the financial statements by providing guidelines on how business transactions are recorded.

To Ensure One Vote Per Person, Please Include the Following Info

While most businesses traditionally report on a quarterly or annual basis, this may not capture the nuances of economic events that do not conform to these neat intervals. For instance, a company may undertake a significant project that spans multiple reporting periods, complicating revenue recognition and expense matching. The time period assumption is a fundamental principle in accounting that allows businesses to divide their complex financial activities into shorter, more manageable intervals, typically monthly, quarterly, or annually.

The Intersection of Time and Revenue Recognition

Investors need to be aware of how the company applies these principles to assess the quality of earnings and the timing of revenue streams. Creditors and lenders also scrutinize financial statements to determine a company’s creditworthiness. The timing of revenue and expense recognition can influence a company’s debt-to-equity ratio, a key metric used by lenders to assess risk. Time period assumptions occur when the company uses different periods than one year to account for its revenues and expenses.

Periodicity Assumption

From an accountant’s perspective, the challenge lies in determining the appropriate cut-off points for expenses and revenues. Deciding how to allocate such costs requires judgment and can lead to inconsistencies if different periods are treated differently. From a company’s viewpoint, adhering to GAAP is crucial for maintaining credibility in the market.

Would you prefer to work with a financial professional remotely or in-person?

- Even though the going concern assumption dictates that businesses should be treated as if they will continue indefinitely, it is helpful to view business performance in shorter time frames.

- Without it, the financial landscape would be devoid of the rhythm and continuity necessary for understanding a business’s financial journey.

- Understanding these cycles is paramount for anyone involved in the financial markets, as they provide a structured way to monitor and evaluate a company’s performance over time.

- The Time Period Assumption requires that the company divides its business activities into equally measured time intervals which are called accounting periods.

Some companies use different time periods to smooth out their earnings or for other accounting reasons. It all depends on your company’s needs and what information you want to convey about your business operations through financial reporting. The time period assumption allows you to acquire timely information on a regular basis about the results of operations of the business in a particular period.

This assumption is crucial because it allows for the periodic reporting of financial information, which is essential for stakeholders to make informed decisions. Unlike other accounting principles that may deal with valuation or recognition, the time period assumption is concerned with the temporal dimension of accounting information. From an accountant’s perspective, the interplay between these two principles is about balancing the need for timely financial information with the requirement for accuracy in revenue recognition. For instance, a business may sign a contract in one accounting period but deliver the goods or services in the next. According to the time period assumption, the business should report any activities that pertain to the current period. However, the realization principle would dictate that revenue from this contract should not be recognized until the goods or services are delivered, even if payment was received in advance.

This assumption is crucial because it provides a structured framework for businesses to present their financial activities in an orderly and understandable manner. Without it, comparing and analyzing financial statements over time would be nearly impossible, as there would be no consistent basis for measurement. The time period assumption is an accounting principle that allows businesses to divide their financial activities into specific time periods, such as months, quarters, or years. The time period assumption in accrual accounting is a fundamental principle that dictates the specific period over which business transactions are reported and analyzed. This assumption is crucial for the preparation of financial statements that reflect a company’s financial performance and position over a defined timeframe. However, the adoption of this assumption carries with it a host of legal and regulatory implications that businesses must navigate carefully.

The time period assumption is a cornerstone of accrual accounting that facilitates the orderly and meaningful presentation of financial information. It allows stakeholders to assess a company’s performance over consistent and regular intervals, providing a temporal framework that is essential for financial analysis, decision-making, and strategic planning. Without it, the financial landscape would be devoid of the rhythm and continuity necessary for understanding a business’s financial journey. Investors and creditors, on the other hand, rely on the time period assumption to make informed decisions. Regular financial reporting periods allow them to track a company’s progress, compare performance across periods, and make projections for the future. Without this assumption, the continuity and periodicity needed to make such analyses would be absent, leaving stakeholders with a fragmented or incomplete financial narrative.

Companies might use just one time period assumption for all their income statements or change the time frame depending on what information is being presented. The time period assumption is a fundamental principle in accounting that dictates how income and expenses are reported on financial statements. It posits that a business’s complex and ongoing activities can be divided into periods of time, such as months, quarters, or years, and that the financial statements can represent the financial results of these periods.

Designed for freelancers and small business owners, Debitoor invoicing software makes it quick and easy to issue professional invoices and manage your business finances. Shareholders always keep an eye on company performance, they will buy more shares if they believe company is on the right track. On the other hand, they will dump the share when the company has poor performance and does not have good planning. The top management needs this information to prepare for the business strategy such as seeking more loans, sell or purchase a new asset, and so on. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

what is an invoice what is it used for is a fundamental concept in accounting that facilitates the accurate and consistent reporting of financial activities. It posits that a business’s complex and ongoing financial activities can be divided into shorter, more manageable intervals, typically monthly, quarterly, or annually. This division allows for the regular and systematic reporting of financial performance and position, enabling stakeholders to make informed decisions based on the most recent data. The length of accounting period to be used for the preparation of financial statements depends on the nature and requirement of each business as well as the need of the users of financial statements.